Every home health agency operating in Illinois, Ohio, Texas, North Carolina, Florida, or Oklahoma faces the same recurring decision: how do you want Medicare to review your claims? The Review Choice Demonstration (RCD) forces that choice on you, and the option you pick has a direct, measurable effect on when cash hits your bank account and how much administrative labor your team absorbs. Choose well and your revenue cycle barely notices the demonstration exists. Choose poorly and you can watch weeks of reimbursement freeze while your billers drown in documentation requests.

This guide breaks down the pre-claim review versus post-claim review decision the way an agency CFO and a compliance director need to see it: cash flow first, administrative burden second, and long-term risk third. Every program detail below is verified against CMS source documentation, because in a Medicare demonstration the difference between a fact and a rumor is the difference between a paid claim and a payment reduction.

What the Review Choice Demonstration Actually Is

The Review Choice Demonstration is a Medicare medical-review program that requires participating home health agencies to demonstrate compliance with coverage and documentation rules before or after their claims are paid. It is administered by the Medicare Administrative Contractor Palmetto GBA, and its purpose is to reduce improper payments in home health while giving agencies a measure of choice in how that review happens. You can read the program overview directly on the CMS Review Choice Demonstration for Home Health Services page.

RCD is not a denial machine in the way agencies sometimes fear. It is a verification framework. The government wants proof that the patient is homebound, that the plan of care is signed and dated, that the face-to-face encounter documentation supports eligibility, and that the services billed are reasonable and necessary. If your documentation already meets those standards, RCD simply confirms what you already do well. If it does not, RCD exposes the gap before or after payment, depending on the review path you selected.

The critical thing to understand is that RCD is a choice architecture. Unlike a blanket prior-authorization mandate, the demonstration lets each agency select the review approach that best fits its documentation maturity, cash position, and staffing. That choice is what this article exists to help you make.

Which States Are in RCD, and What Changed in June 2024

RCD applies to home health agencies that bill Medicare in six demonstration states: Illinois, Ohio, Texas, North Carolina, Florida, and Oklahoma. If your agency serves patients and submits claims in any of these states, RCD participation is mandatory, not optional.

In 2024, CMS extended the demonstration for an additional five years. Per the CMS program page, the extended demonstration began June 1, 2024 and is scheduled to run through May 31, 2029. This is not a program winding down. Agencies planning their revenue cycle strategy should treat RCD as a fixed feature of the operating landscape through the rest of the decade.

The June 2024 extension also carried a structural change that reshapes the pre-claim versus post-claim decision. CMS removed the old "Minimal Review with 25% Payment Reduction" option from the initial choice selections. Agencies that were sitting in that option were contacted by Palmetto GBA to make a new selection. As a result, the two initial choices every agency now weighs are Pre-Claim Review and Postpayment Review. That removal matters for your decision, and we cover why below.

The RCD Choice Menu: Your Options Explained

RCD splits into two tiers. There are the initial choices every participating agency selects at the start of a cycle, and there are the subsequent choices an agency unlocks only after it proves sustained accuracy. Understanding both tiers is essential, because the initial choice you make is really a decision about how quickly you can graduate to the lighter-touch subsequent options.

Choice 1: Pre-Claim Review (PCR)

Under pre-claim review, your agency submits the supporting documentation for a home health period of care before you submit the final claim for payment. Palmetto GBA reviews that documentation and issues an affirmation decision. When a request is affirmed, you receive a Unique Tracking Number (UTN) that you attach to the final claim. A claim submitted with a valid, affirmed UTN is excluded from further medical review and moves through the payment system cleanly.

Pre-claim review is a front-loaded model. You do the compliance work up front, get a decision from Medicare, and then bill with confidence. The trade-off is that you cannot bill the final claim until you have your affirmation and UTN in hand, which introduces a timing dependency into your revenue cycle. The details of the PCR submission and UTN process are documented in the CMS RCD Operational Guide.

Choice 2: Postpayment Review

Under postpayment review, your claims are paid first through the normal process, and Palmetto GBA reviews the documentation after payment. The review happens through Additional Documentation Requests (ADRs): after your claim is paid, the contractor asks for the medical records, you submit them, and the reviewer confirms whether the claim was payable. If the documentation does not support the claim, the payment can be recouped.

Postpayment review is the default. Per CMS guidance, an agency that does not actively make an initial choice selection by the deadline is automatically placed into Choice 2: Postpayment Review. It preserves your near-term cash flow because you get paid before the review, but it defers risk: an unfavorable postpayment finding means giving money back, sometimes months after you recognized the revenue.

The Retired Choice: Minimal Review with 25% Payment Reduction

Before June 2024, agencies could elect a "Minimal Review with 25% Payment Reduction" option. Under this path, an agency accepted an automatic, non-appealable 25% cut to its Medicare payment in exchange for being largely exempt from the demonstration's medical review. As confirmed on the CMS program page, CMS removed this option from the initial choice selections as part of the five-year extension.

The removal is instructive. That 25% reduction was, in effect, the price CMS attached to opting out of documentation review, and it was steep enough that very few agencies chose it. For any agency running the numbers, a permanent 25% haircut on Medicare revenue almost never beats the cost of simply doing the documentation work correctly under pre-claim or postpayment review. The lesson carries into your current decision: there is no cheap way to avoid the review. The only durable strategy is documentation accuracy.

Subsequent Choices: What You Unlock at 90%

Here is where the demonstration rewards good performers. If your agency achieves a full affirmation rate or claim approval rate of 90% or greater over a six-month period (based on a minimum of 10 submitted pre-claim review requests or claims), you become eligible to move to one of the lighter subsequent review choices, as described in CMS guidance. Those subsequent options include:

- Continue Pre-Claim Review for another cycle if you prefer the certainty of up-front affirmation.

- Selective Postpayment Review, where Medicare reviews only a sample of your claims after payment rather than requiring up-front review of every episode.

- Spot Check Review, where roughly 5% of your claims are reviewed every six months to confirm continued compliance.

An agency that reaches the 90% threshold but does not actively select a subsequent option is placed by default into Selective Postpayment Review for the remainder of the demonstration. The strategic takeaway is that the 90% affirmation rate is the gateway to a dramatically lighter administrative load. Everything in your initial-choice decision should be oriented toward hitting it.

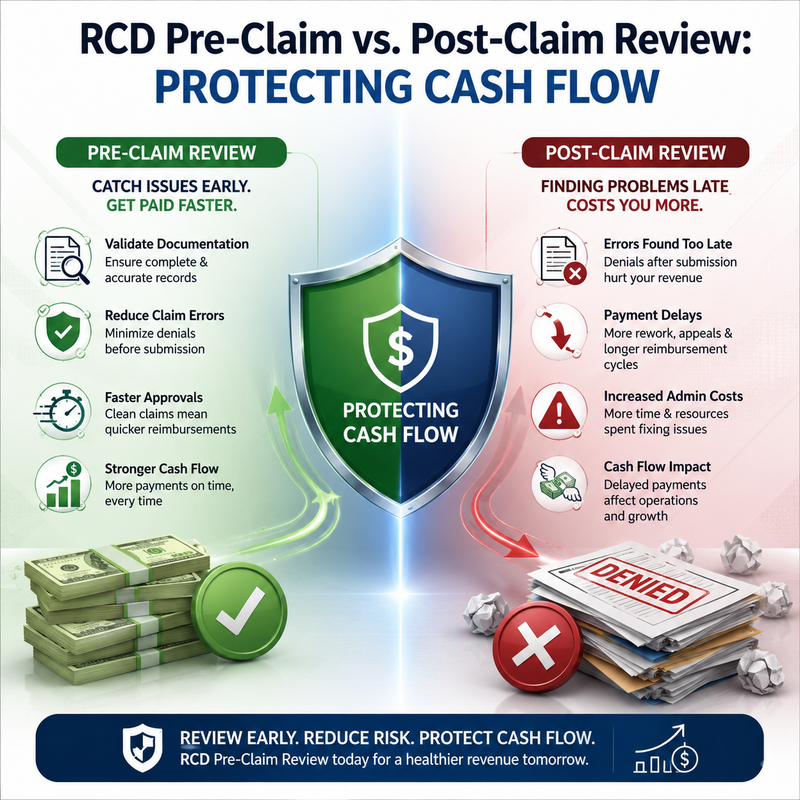

Pre-Claim vs. Post-Claim: The Cash Flow Math

For most agencies, the pre-claim versus post-claim decision is fundamentally a cash flow decision, so let us treat it as one.

Pre-claim review delays the start of billing but protects the certainty of payment. Because you must obtain an affirmation and UTN before submitting the final claim, there is a lag between the end of the care period and the moment you can bill. If your submission and affirmation turnaround is tight, that lag is modest. If your team submits late or your documentation triggers a non-affirmation and resubmission, the lag compounds and days in accounts receivable climb. The upside is that once you hold an affirmed UTN, that revenue is effectively locked. You are not carrying the risk that a paid claim gets clawed back later.

Postpayment review protects near-term cash but leaves a recoupment tail. Under Choice 2, claims are paid on the normal cycle, so your immediate cash position looks healthier. The catch is that the review still happens, only later, through ADRs after payment. If those reviews go against you, the recoupment hits a future period, often when you have already spent or forecasted the revenue. In accounting terms, postpayment review converts a timing question into a reserve question: how much of your recognized Medicare revenue might you have to give back?

The honest answer for most agencies is that the "right" cash flow choice depends on two variables: how clean your documentation already is, and how much working capital you hold. A well-documented agency with a strong affirmation history often finds pre-claim review barely dents its cash cycle while eliminating recoupment anxiety. A cash-tight agency with shakier documentation may lean toward postpayment review to preserve liquidity, while accepting that it is deferring, not avoiding, the risk. Getting this balance right is exactly the kind of problem a mature revenue cycle management operation is built to solve.

Pre-Claim vs. Post-Claim: The Administrative Burden

Cash flow is only half the equation. The two paths distribute administrative work very differently across time.

Pre-claim review front-loads the labor. Every single episode requires a documentation package assembled and submitted before billing, and every submission is a discrete task your team must track through to affirmation. The workload is predictable and continuous. The advantage is that the work is visible and controllable: you know exactly what is outstanding, and a clean submission process keeps the pipeline flowing.

Postpayment review back-loads the labor into ADR responses, and that work is spikier and less predictable. ADRs arrive on the contractor's schedule, not yours, and each carries a hard deadline to produce records. A batch of ADRs landing in the same week can overwhelm a small billing team, and a missed ADR deadline can convert a payable claim into a denial and recoupment. The burden is lower on average but riskier at the peaks.

There is also a documentation-quality dimension that both paths share. Whether the review is up front or after the fact, the reviewer is checking the same things: homebound status, medical necessity, a signed and dated plan of care, and face-to-face encounter documentation that supports eligibility. Agencies that invest in a disciplined home health review process, catching documentation gaps before claims are ever built, perform well under either RCD path because they are feeding the reviewer complete records every time.

The 90% Affirmation Threshold: Your Path to Lighter Review

If there is a single number to organize your RCD strategy around, it is 90%. Reaching a full affirmation or approval rate of 90% or greater over a six-month period is what unlocks the lighter subsequent review choices, and staying above it is what keeps you there. Below that line you remain in full review; above it you earn selective or spot-check review and reclaim a large share of your team's time.

Hitting 90% is not about gaming the reviewer. It is about documentation completeness and accuracy at the source. The affirmations you want come from records that unambiguously establish:

- Homebound status, documented in clinical terms that show why leaving home requires considerable and taxing effort.

- Medical necessity, with the skilled need clearly tied to the plan of care.

- A signed, dated plan of care that matches the services billed.

- Face-to-face encounter documentation that supports the certification of eligibility and connects the encounter to the primary reason for home health.

- Timely, legible physician signatures on every required order and certification.

The agencies that consistently clear 90% treat documentation as a front-end discipline, not a back-end scramble. They audit the chart before the claim exists, they coach clinicians on the specific language reviewers look for, and they build a feedback loop from every non-affirmation back into their intake and coding process. That is precisely the improvement arc documented in our case study on RCD claim approval improvement, where tightening documentation and pre-submission review moved an agency's affirmation performance into the range that unlocks lighter review.

How to Choose: A Decision Framework for Your Agency

There is no universally correct answer, but there is a correct answer for your agency at this moment. Work through these questions in order.

Start with your documentation track record

If your agency already produces clean, complete documentation and has a history of high approval rates, pre-claim review is usually the stronger long-term play. You will affirm at a high rate, your UTNs will flow, and you will lock in payment certainty while marching toward the 90% threshold that unlocks lighter review. Pre-claim review turns your existing documentation strength into a cash-protection advantage.

Weigh your working capital

If your agency is cash-tight and cannot comfortably absorb a billing lag while you build a clean pre-claim submission process, postpayment review preserves near-term liquidity. Just go in with eyes open: you are choosing to carry recoupment risk into future periods, so you should reserve against it and invest immediately in documentation quality to shrink that risk.

Assess your team's capacity for predictable vs. spiky work

Pre-claim review demands steady, continuous submission discipline. Postpayment review demands the ability to respond to unpredictable ADR spikes on tight deadlines. Match the path to how your team actually works, or to the operating partner you bring in to handle it.

Orient everything toward 90%

Whichever initial path you choose, treat the 90% affirmation threshold as the real goal. The initial choice is a stepping stone; the subsequent selective or spot-check review is the destination where your administrative burden drops sharply. A path that gets you to 90% fastest is usually the right path, even if it costs a little in near-term cash or up-front labor.

Where an RCM and Clinical Partner Changes the Math

The reason many agencies struggle with the pre-claim versus post-claim decision is that both paths expose the same underlying weakness: documentation that is not consistently review-ready. Fix that, and the choice becomes far less stressful, because you affirm at a high rate under either path and quickly earn your way into lighter review.

That is where an integrated partner earns its keep. A team that combines clinical documentation review, OASIS and coding accuracy, and disciplined billing can raise your affirmation rate toward the 90% threshold, manage PCR submissions or ADR responses so deadlines never slip, and turn every non-affirmation into a process fix rather than a repeat error. Medeoan's home health review and revenue cycle management services are built specifically for agencies operating under RCD in the six demonstration states, and the affirmation-rate gains that path can produce are illustrated in our RCD claim approval improvement case study.

The RCD decision is not really pre-claim versus post-claim. It is whether your documentation is strong enough that the choice barely matters. Build that strength, and RCD stops being a threat to your cash flow and becomes a competitive advantage over agencies that never got their documentation house in order.

Frequently Asked Questions

What is the Review Choice Demonstration for home health?

The Review Choice Demonstration (RCD) is a Medicare medical-review program, administered by Palmetto GBA, that requires participating home health agencies to demonstrate compliance with coverage and documentation rules either before or after their claims are paid. It gives agencies a choice in how that review happens, with the goal of reducing improper payments. Full details are on the CMS RCD program page.

Which states are part of RCD?

RCD applies to home health agencies that bill Medicare in six states: Illinois, Ohio, Texas, North Carolina, Florida, and Oklahoma. Participation is mandatory for agencies submitting claims in these states.

What is the difference between pre-claim review and postpayment review?

Under pre-claim review (Choice 1), you submit supporting documentation and receive an affirmation and a Unique Tracking Number (UTN) before you bill the final claim, so review happens up front. Under postpayment review (Choice 2), claims are paid first and then reviewed afterward through Additional Documentation Requests. Pre-claim review protects payment certainty but adds a billing lag; postpayment review protects near-term cash but carries recoupment risk.

What affirmation rate do I need to move to lighter review under RCD?

You need a full affirmation rate or claim approval rate of 90% or greater over a six-month period, based on a minimum of 10 submitted pre-claim review requests or claims. Meeting that threshold makes you eligible for the subsequent, lighter review options such as selective postpayment review or spot check review, per CMS guidance in the RCD Operational Guide.

What happens if I do not choose an RCD option?

If your agency does not actively make an initial review choice selection by the deadline, CMS places you by default into Choice 2: Postpayment Review. If you have already reached the 90% affirmation threshold but do not select a subsequent option, you are defaulted into Selective Postpayment Review for the remainder of the demonstration.

Was RCD extended, and when does it end?

Yes. CMS extended the demonstration for five additional years. The extended demonstration began June 1, 2024 and is scheduled to run through May 31, 2029, as noted on the CMS RCD program page. Agencies should plan their revenue cycle strategy around RCD being in place through 2029.

What is the 25% payment reduction, and is it still an option?

The 25% payment reduction was tied to the old "Minimal Review with 25% Payment Reduction" choice, under which an agency accepted an automatic, non-appealable 25% cut to its Medicare payment in exchange for minimal medical review. CMS removed that option from the initial choice selections as part of the June 2024 five-year extension, so it is no longer available as an initial choice. Agencies now choose between pre-claim review and postpayment review.

What is a Unique Tracking Number (UTN)?

A UTN is the identifier Palmetto GBA issues when a pre-claim review request is affirmed. You attach the UTN to your final claim, and a claim submitted with a valid affirmed UTN is excluded from further medical review, allowing it to process cleanly through the payment system. The UTN submission format is detailed in the CMS RCD Operational Guide.

Which RCD choice is better for cash flow?

It depends on your documentation quality and working capital. Postpayment review preserves near-term cash because you are paid before review, but it defers recoupment risk into future periods. Pre-claim review adds a short billing lag but locks in payment certainty once you hold an affirmed UTN. Agencies with strong documentation and adequate working capital often find pre-claim review protects cash flow better overall by eliminating clawbacks, while cash-tight agencies may prefer postpayment review in the near term. A strong revenue cycle management process makes either path work by driving your affirmation rate toward the 90% threshold.

How can a home health agency improve its RCD affirmation rate?

Focus on documentation completeness at the source: clearly document homebound status and medical necessity, ensure a signed and dated plan of care that matches billed services, secure face-to-face encounter documentation that supports eligibility, and obtain timely physician signatures. Auditing charts before claims are built and feeding every non-affirmation back into your intake and coding process is what consistently moves agencies above 90%, as shown in our RCD claim approval improvement case study.